ANTHROPIC Tender Offer Planning Guide

Your Anthropic Equity Is Worth More Than You Think.

The decisions you make in the next few days determine how much you keep.

Navigate Tomorrow. Prosper Today.

prosperowealth.com

Section 1

Why This Tender OFFER MATTERS

You've been doing the math in your head. The numbers are real. The window is short.

Which shares you sell — and which you keep — could represent a six-or-seven-figure difference in what you take home. Not over a career. In this transaction.

This guide covers the tax mechanics by equity type, the withholding gap most employees don't see coming, and strategies that can change the math before the tender window opens.

Selling isn't a bet against Anthropic. It's making sure your income, your career, and your net worth aren't all one bet.

Prospero Wealth · For educational purposes only. Not personalized investment or tax advice.

Section 2

How This Tender Offer Works

A tender offer is a company-organized opportunity to sell a portion of your vested equity to institutional investors at a set price, before a public listing. It's SEC-regulated, typically open for approximately 20 business days, and structured as a single transaction at a uniform price.

Three things make this different from selling public stock: the price is fixed (no market fluctuation during the window), volume is capped (there are limits on how many shares or how much dollar value you can sell), and the window is short.

The Process

01

Sign Documents

NDA, W-9, and tender participation agreement via the platform.

02

Select & Submit

Choose which shares and how many. Confirm bank details for wire.

03

Window Closes

~20 business days. Orders finalized, transaction settles.

04

Proceeds Arrive

Typically 2–4 weeks after close. Taxes withheld at source.

A note on timing: Three weeks sounds like enough, but if you're heads-down shipping, it passes fast. The mechanical steps aren't complex — the planning decisions behind which shares to sell and how to prepare for the tax impact benefit from lead time. Get your order in early.

Prospero Wealth · For educational purposes only. Not personalized investment or tax advice.

Section 3

Anthropic grants employees different types of equity, and each carries different tax treatment, different costs, and different planning opportunities. Employees who joined at different stages face genuinely different situations — and the company is in a transition period that makes this especially relevant.

Earlier employees received primarily stock options at lower strike prices. More recent hires may have RSUs, options at higher strikes, or a mix of both. As the valuation has climbed, the economics of each grant type have shifted. Understanding what you hold is the prerequisite for every decision that follows.

ISOs

Ownership

Not until exercised

Your cost

Strike price × shares

Tax at exercise

No regular tax (AMT may apply if held)

Tax at sale

Key lever

Holding period → LTCG rates; AMT modeling

NQSOs

Ownership

Not until exercised

Your cost

Strike price × shares

Tax at exercise

Ordinary income on full spread

Tax at sale

Cap gains on post-exercise appreciation only

Key lever

Straightforward — limited planning levers

RSUs (Double-Trigger)

Ownership

Auto on both triggers met

Your cost

None

Tax at vest

Ordinary income on full FMV

Tax at sale

Cap gains on post-vest appreciation

Key lever

Withholding gap; concentration management

ISOs in a Tender: The Qualifying vs. Disqualifying Decision

This is the most commonly misunderstood aspect of using ISOs in a tender offer. If you exercise ISOs and sell immediately — a same-day transaction — you won't meet the qualifying disposition holding periods (more than 1 year from exercise and more than 2 years from grant). The spread is taxed as ordinary income, just like an NQSO. The ISO's potential tax advantage is lost.

If you’ve previously exercised ISOs and held the shares long enough to meet both holding periods, the gain may qualify for long-term capital gains rates (which could potentially be much lower than ordinary income tax rates that you might otherwise pay).

AMT may apply at the time of exercise if ISOs are exercised and held. The figures above are simplified illustrations; actual tax outcomes depend on your complete income picture, filing status, and state of residence. Consult a qualified tax professional.

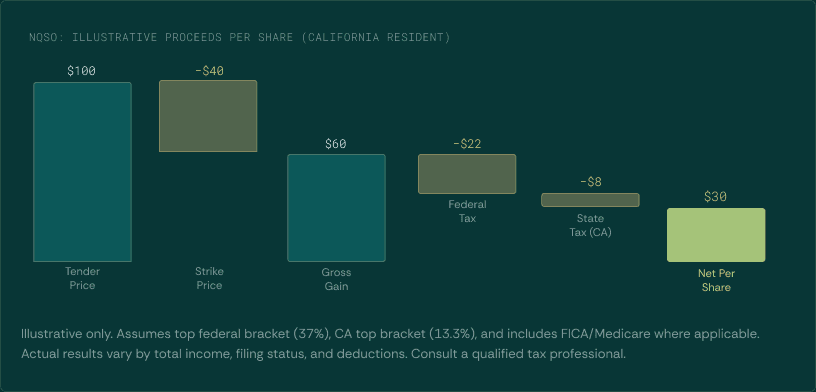

NQSOs: What You Actually Take Home

Your net value from the tender is not the tender price per share. It's the tender price minus your strike price, minus taxes. The platform handles a "cashless exercise" — it loans you the cost to exercise, sells to the buyer, and sends you the net. But many employees overestimate their proceeds because they're looking at the gross share price, not the spread.

RSUs: The Double-Trigger Question

You don't face exercise decisions or out-of-pocket costs with RSUs. But you also have fewer planning levers. The main risk is the withholding gap: your employer withholds at a formulaic rate that may be lower than your actual marginal rate in a high-income year.

At private companies, RSUs typically require both time vesting and a liquidity event to settle. Whether this tender offer qualifies as the second trigger depends on Anthropic's specific plan terms. If it does, your vested RSUs would settle at the tender price — and the full value is taxed as ordinary income at that point.

Prospero Wealth · For educational purposes only. Not personalized investment or tax advice.

Section 4

How much to sell and which shares

The mechanics of submitting an order are straightforward. The planning behind which shares to select, how much to sell, and what that means for your broader financial picture is where thoughtful analysis creates real value.

This may be the nearest-term opportunity to convert paper wealth into real dollars. While Anthropic has taken steps consistent with IPO preparation, timelines are inherently uncertain. Previous tender offer prices at other companies have occasionally exceeded eventual IPO prices. Certainty has value.

The Case for Participating

Selling a portion still leaves you with substantial upside. If the tender permits selling 10% of your vested position, you retain 90%+ exposure to future appreciation. This isn't an exit — it's partial liquidity.

Cash from the tender creates planning opportunities beyond the obvious emergency fund or down payment — including, in some cases, funding ISO exercises that start the clock toward more favorable tax treatment at a future liquidity event.

Which Shares to Select

The order matters. For employees holding multiple equity types, the tax treatment differs dramatically depending on which lots you sell. Here's the hierarchy:

What equity do you hold?

Only RSUs or only NQSOs

Straightforward: decide what percentage to sell and proceed. Tax treatment (ordinary income) is the same regardless of which lots you choose.

Tax: Ordinary income rates on full amount

Mix of NQSOs + ISOs (never exercised)

Sell the NQSOs in the tender. Using ISOs in a same-day sale creates a disqualifying disposition — they'd be taxed as ordinary income anyway. Preserve ISOs for a future exercise-and-hold strategy.

Tax: Ordinary income on NQSO spread; ISOs preserved

Previously exercised ISOs (held 1yr+ / 2yr+)

These may qualify for long-term capital gains treatment. If selling in the tender, these are often your most tax-advantaged shares

Tax: ~23.8% federal (LTCG) vs. up to 37% (ordinary)

Potentially QSBS-eligible shares

If held 5+ years and the company qualifies, Section 1202 may allow excluding some or all gain from federal tax. Strict rules — investigate before selling.

Tax: Potentially $0 federal on qualifying gain

Individual circumstances vary significantly. Holding period calculations, QSBS eligibility, and tax treatment should be verified with a qualified tax professional before making lot selections on the tender platform.

Prospero Wealth · For educational purposes only. Not personalized investment or tax advice.

Section 5

The tax Reality

The withholding that comes out of your tender proceeds is not the same as your actual tax bill. Understanding the gap before you spend the proceeds is essential.

The Withholding Gap

You may want to consult with your tax preparer to ensure that you are paying safe harbor estimated taxes for the year to avoid tax penaties from under-withholding. Your employer will withhold taxes from the tender proceeds at the federal supplemental rate: 22% on the first $1M of supplemental wages, 37% on amounts above $1M. State withholding varies. But if the tender pushes your total income well above your normal bracket — which it almost certainly does — the blended withholding may understate your actual marginal rate.

Run a tax projection — before or immediately after the tender

A tax projection models your full-year income (salary, tender proceeds, any other equity events), calculates your actual marginal rate, compares it to what's been withheld, and identifies the gap. This is standard practice for anyone experiencing a significant income spike. Don't wait until April.

Prospero Wealth · For educational purposes only. Not personalized investment or tax advice.

Section 6

Strategies That May Change the Math — Especially looking ahead

Most tender offer guidance stops at the tax section. Participate, pay your taxes, invest the rest. That misses the most important planning opportunity: what you put in place now doesn't just affect this tender—it positions you for future tender offers and the IPO.

The strategies below aren't about what to do with proceeds after they land. They're tools that can reduce the effective tax rate on this transaction, generate ongoing tax benefits across future liquidity events, and — in some cases — produce investment returns above the benchmark while doing it.

$600K illustrative gain → ~$288K expected tax

What strategies should you consider post-exercise?

Custom Direct Indexing

Harvest losses from individual stock positions to offset gains. Highest loss-generation potential in year 1.

Tax-Aware Long/Short Portfolios

Starts with direct indexing but adds long and short extensions, drastically increasing tax loss harvesting capabilities and providing for possibility of upside alpha above your selected benchmark.

Fund Future ISO Exercises

Use tender cash to exercise ISOs, start qualifying disposition clock for future event at LTCG rates.

Charitable Giving (Appreciated Shares)

Donate appreciated shares to DAF — eliminate cap gains + income tax deduction in a high-income year.

Opportunity Zone Investments

Defer capital gains tax; potential exclusion of OZ appreciation after 10+ years. Applies to capital gains, not ordinary income.

Direct Indexing: A Foundational First-Step

Instead of holding a broad index fund, a direct indexing strategy owns hundreds, perhaps thousands, of individual stocks in a separately managed account, designed to track its index benchmark. Because each position is held individually, losses are harvested independently — even while the overall portfolio appreciates.

Those realized losses offset capital gains elsewhere in your portfolio. In the first year, the harvesting opportunity is typically highest as individual stocks drift from purchase prices. Over time, in a long-only portfolio, the opportunity diminishes as the broad market rises and most positions sit above their cost basis.

Direct indexing is a strong starting point for most portfolios. But for employees facing the scale of taxable events that come with Anthropic equity, it may not be enough on its own.

You may already be familiar with direct indexing. Perhaps you’re already using it. We’ve seen and worked with a number of direct indexing providers, and can say that track records and performance vary. When evaluating direct indexing providers, here are some the questions we ask: How often do they harvest losses? Is there a set cadence, or are they opportunistic? What kind of benchmarks do they offer? Just US large cap, or broader, global indexes? How closely do they track their index? Do they seek to provide alpha above the benchmark, and if so, how? What’s their historical track record?

Long/Short: Generating Losses to Offset Gains

A more concrete example: for a California resident in the highest bracket, the combined short-term tax rate on ordinary income and short-term gains potentially can exceed 50%. The highest long-term capital gains rate is roughly 37% (in CA). That's a big difference on its own. What's even more exciting is that capital gains can be neutralized, in many cases, with offsetting losses, as in a long-short strategy. Planned correctly, a long-short strategy can reduce (or entirely defer) capital gains. More money compounding now means more money for you to access later.

This is where the planning gets meaningfully more sophisticated — and where the tax impact can be dramatically larger.

A long-short extension strategy starts with the same foundation as direct indexing: investing 100% of your capital in a diversified portfolio tracking a benchmark like the ACWI Global Index. However, it then extends the portfolio through borrowing to take additional long positions in stocks expected to outperform, and shorting an equal amount in stocks expected to underperform.

For example, a 130/30 portfolio would invest 30% of your original investment in short positions, and another 30% in long positions. With a $100 investment, your net market exposure stays at $100 (neutral beta), but your gross exposure is $160 (with the $30 short and $30 long extensions ) — meaning there are substantially more positions generating harvestable losses. See a more thorough overview here.

This structure delivers three distinct advantages over long-only direct indexing:

1. Substantially More Tax Losses to Offset Gains

The long and short extensions both generate harvestable losses. In a rising market, short positions that are covered create realized losses even when long positions are appreciated. Research shows 130/30 strategies may generate tax alpha several multiples higher than long-only — and the benefit persists longer rather than tapering off after year one.

2. Potential for Alpha Above the Benchmark

Because an alpha model drives which stocks to overweight and underweight, the strategy has the potential to generate pre-tax returns above the benchmark—not just tax benefits. Total alpha is the sum of tax alpha and pre-tax alpha. Long-only direct indexing, by design, doesn't attempt to outperform.

3. More Effective Concentrated Position Selldowns

A long-short portfolio can be funded directly with a concentrated position (e.g., maybe you have some NVDA you bought a few years ago in a brokerage account). The losses generated can be used to offset gains as you diversify out — potentially achieving tax-neutral diversification over several years.

Tax-loss harvesting and long/short strategies involve risks including market risk, short selling risk, leverage risk, and active management risk. Losses harvested may defer but do not eliminate tax liability. The wash sale rule and other limitations apply. Past tax outcomes from simulations are not indicative of future results. These strategies are not suitable for all investors. Consult a qualified tax and investment professional.

The Multi-Year Play: Using the Tender to Fund ISO Exercises

This is directly connected to the tender decision and deserves emphasis. If you participate in the tender — generating cash and ordinary income — you may be able to use a portion of those proceeds to exercise ISOs separately, starting the clock toward qualifying disposition treatment for a future liquidity event like an IPO.

That future qualifying disposition would be taxed at long-term capital gains rates rather than ordinary income — a difference of roughly 13–17 percentage points depending on your state. The trade-off: exercising ISOs and holding creates AMT exposure, and you're spending cash on illiquid shares. But for employees with low-strike ISOs and a reasonable expectation of a future liquidity event, this is a lever worth modeling.

Other Strategies Worth Considering

Charitable giving with appreciated shares. If philanthropy is part of your plan, donating appreciated shares to a donor-advised fund can eliminate the capital gains tax on those shares while providing an income tax deduction at fair market value. Especially tax-efficient in a high-income year like a tender year.

Opportunity Zone investments. Capital gains invested in a Qualified Opportunity Zone fund within 180 days of realization can defer the tax on those gains. If held 10+ years, gains on the OZ investment itself may be excluded from federal tax. Most relevant for employees realizing capital gains (not ordinary income) — so applies more directly to qualifying ISO dispositions or previously exercised shares.

This isn't just about one tender

The strategies you put in place now — a long/short portfolio generating losses, ISOs exercised and counting toward qualifying disposition, a direct indexing foundation building tax assets — position you for the entire sequence of events ahead: this tender, potential future tenders, and the IPO. The question isn't "should I sell in the tender?" It's "what infrastructure do I build now so that every future liquidity event is more tax-efficient than the last?"

Prospero Wealth · For educational purposes only. Not personalized investment or tax advice.

Section 7

The Coordination problem

Here's what we see consistently with employees at companies like Anthropic: smart, analytically rigorous people who have the right professionals in their orbit — a CPA, maybe an estate attorney, perhaps a financial advisor from a previous chapter — but no one coordinating between them.

Your CPA doesn't know you're considering exercising options in Q4. Your estate attorney doesn't know about the tender. If you have an existing financial advisor, they may not understand how equity compensation intersects with the tax projection, the estate plan, and the investment strategy. Each professional does their job well in isolation, but no one is looking at the full picture.

The result is missed opportunities, unnecessary tax exposure, and a financial life that feels fragmented. The ISO exercise that should have been timed alongside the tender gets deferred. The charitable gift that would have been maximally efficient in a high-income year gets made in a lower-income year. The withholding gap doesn't get caught until April.

The value of an advisor in this context isn't secret information. It's having someone who coordinates the CPA, the estate attorney, and the investment strategy around a unified plan — and who understands equity compensation deeply enough to translate between the technical details and the life decisions.

Next Steps

Let's Talk

If you're evaluating your Anthropic tender offer and want a second opinion, we're happy to have the conversation. No obligation, no sales pressure.

A conversation with us typically covers three things: a review of your equity position and which lots make sense for the tender, a preliminary tax projection for the tender year, and an honest assessment of whether working together fits your situation.

Our advisors are former tech professionals who've been on your side of the equity comp decisions. We understand both the technical planning and the emotional weight of these choices.

Schedule a Conversation

30 minutes. Your equity position, your questions, straight answers.

Disclosures

This guide is for educational purposes and does not constitute personalized investment, tax, or legal advice. The information provided is based on publicly available data and general tax principles as of the date of publication. Tax laws and regulations are complex and subject to change. Individual circumstances vary significantly, and the strategies discussed may not be appropriate for your specific situation.

Prospero Wealth is a registered investment advisor. Registration with the Securities and Exchange Commission does not imply a certain level of skill or training.

Any hypothetical examples, illustrative figures, or scenarios presented in this guide are for educational purposes only and do not represent actual client outcomes. Past results are not indicative of future performance. No guarantees are made regarding tax outcomes or investment returns.

Consult a qualified tax professional, attorney, and financial advisor for advice specific to your situation before making any investment or tax planning decisions.

Prospero Wealth · Navigate Tomorrow. Prosper Today.